Humber Refinery gigafactory: Britain's best-kept industrial secret is an unexpected solution to saving the planet

This is the very image of the country's fossil fuel industry, a mammoth plant that churns out petrol, aviation fuel and other such products. It is a spaghetti junction of pipes - thousands of miles of shiny steel tubes snaking from canister to tank and back again.

Everywhere you look there are chimneys belching steam and fumes, others occasionally flaring with flames that light the winter sky.

The air is thick with the acrid whiff of hydrocarbons, the ground black with carbon soot. It looks and smells like a vision of the very thing we're trying to escape.

But here's the thing. This refinery - chimneys, flares, carbon emissions and all - is actually a crucial part of our escape route. If we are to eliminate carbon emissions in this country it will be partly thanks to what happens in this place.

The Humber Refinery is one

of the most important links in the supply chain for the most important

product of the green industrial revolution

The Humber Refinery is one

of the most important links in the supply chain for the most important

product of the green industrial revolution

Perhaps that seems implausible - sacrilegious even - but it is also the practical reality of confronting climate change. For it turns out the route to net zero is far more complex and nuanced than many might have you believe.

Eliminating greenhouse gas emissions will almost certainly mean doing much of the stuff you're doubtless familiar with: planting more forests and sequestering more carbon; weaning ourselves off fossil fuels for electricity; recycling more - a lot more; using renewable power and electric cars; reducing our demand for energy by insulating our homes and improving the efficiency of industrial processes.

But it will also feature aspects we might be a little less comfortable with: digging vast quantities of stuff out of the ground, racing to secure resources before other countries do; and relying on oil refineries like this, both in the short term and potentially the long term too.

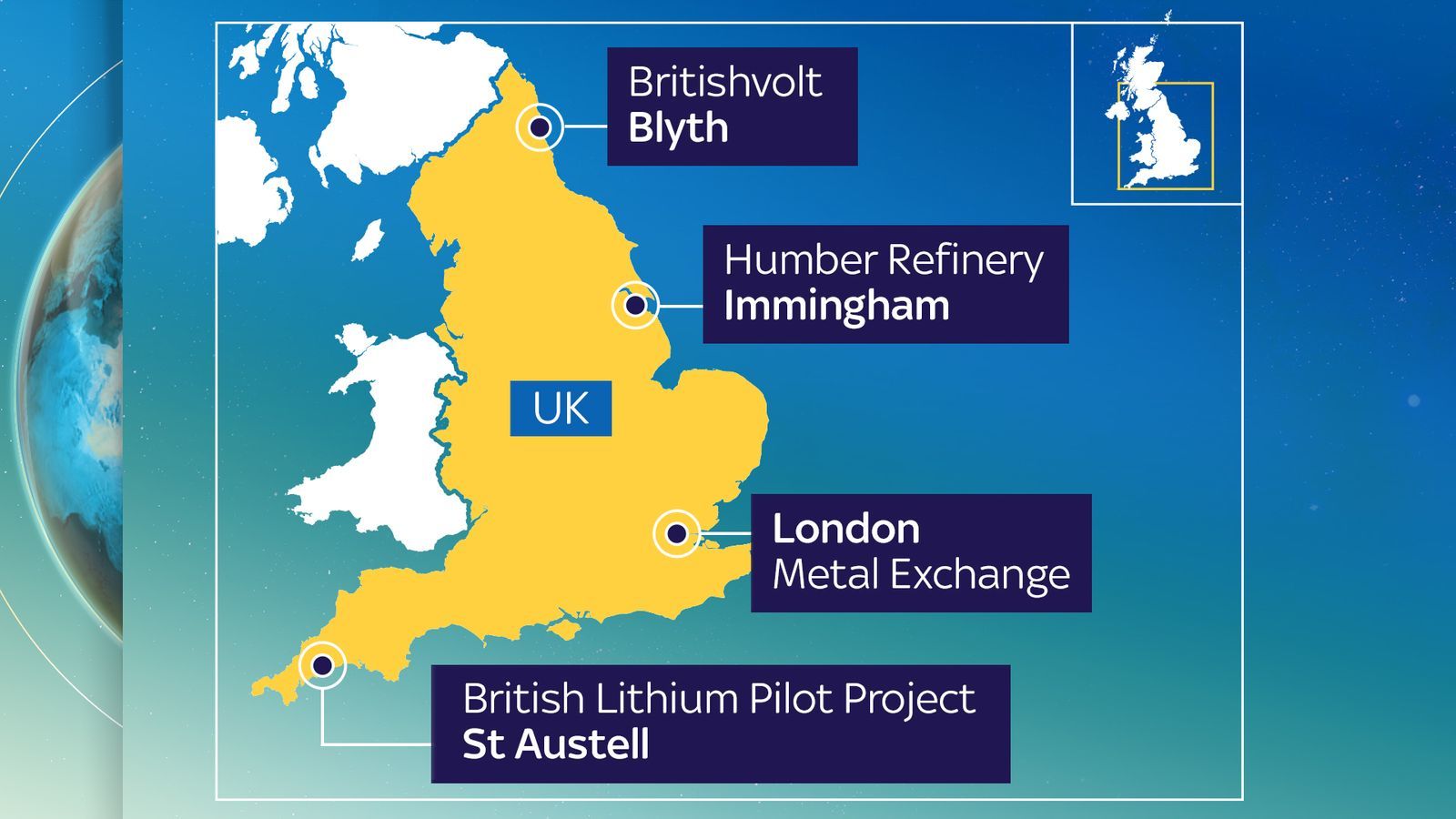

Four locations with a stake in the UK's battery powered future

Four locations with a stake in the UK's battery powered future

If this might all sound a little unsettling then it's primarily because when it comes to net zero and how we get there, there are actually two versions of the story: the one the politicians like to talk about and then the one they prefer not to mention. This is about the second version of the story.

But before we get to that, let's sneak a peek at that other, more acceptable story.

Britishvolt - the gigafactory in Blyth

Just over a hundred miles north of the Humber Refinery is the town of Blyth. Here on the glorious Northumberland coast, at a site which was once the coal store for a now defunct power station, work is under way on one of the most important projects in contemporary UK industrial history.

This is the site where Britishvolt, a battery startup, is building its gigafactory. Precisely what constitutes a gigafactory is one of those questions without a very clear answer (especially since it's originally a kind of branding term coined by the mercurial entrepreneur Elon Musk) but in broad terms it means a very big battery factory.

An artist's impression of the Britishvolt gigafactory in Blyth

An artist's impression of the Britishvolt gigafactory in Blyth

At this stage it's worth noting three important principles when it comes to the green energy transition.

The first is that we are unlikely ever to eliminate greenhouse gas emissions without making a staggering number of batteries. We need batteries for energy storage to counter the inherent intermittency of renewable power sources like wind and solar. We'll need them for our homes. Most of all, we'll need them for our cars.

The second principle is that the onset of the electrical age turns the industrial hierarchy of the car business on its head. In the internal combustion engine era - which is to say the past century and a bit - the single most important part of a car was its engine. But in the electric era the most valuable part of a car is likely to be the battery.

This might sound like superfluous detail until you recall that much of this country's motoring expertise and heritage is bound up in engine design and production. Battery manufacture, on the other hand, is something which at present happens mostly elsewhere.

Consider: when Jaguar Land Rover built its new all-electric Jaguar I-Pace car this British-designed car was actually contracted out to a plant in Austria.

The great fear of the motoring industry, and the government, is that something similar happens with all UK car manufacture in future with hundreds of thousands of jobs being lost as engine manufacture goes the way of the dodo.

Jaguar's all electric I-Pace car

Jaguar's all electric I-Pace car

The third and final principle comes back to Brexit. In four years' time, impending trade rules will change the definition of what constitutes something that, for the purposes of tariffs and quotas, is "made in the UK".

These "Rules of Origin" dictate that by 2027 at least 55% of a finished car's value must be derived from either the UK or the EU, or the car may face significantly higher export tariffs. Given the battery is the most valuable part of an electric car, it is suddenly all-important to make them locally.

All of which is why there is so much focus on Britishvolt. Ministers, including Business Secretary Kwasi Kwarteng, have lavished this place with attention and publicity, heralding it as the saviour for the British motor industry, and a symbol of this country's green potential.

Electric car batteries produced by Britishvolt

Electric car batteries produced by Britishvolt

It's worth noting that the factory here will not be the only such plant in the UK. Chinese battery maker Envision already produces a significant number of batteries for Nissan (currently just under two gigawatt hours (GWh) a year) in its Sunderland factory. It has pledged to increase that to as much as 38 GWh.

Those batteries are committed to Nissan but the Britishvolt plant, which aims to produce 30 GWh, will make batteries for various other firms on contract.

Put those two plants together and the UK would be two thirds of the way towards the likely target of the roughly 90 GWh battery production it needs to replace internal combustion engine manufacture for the domestic car industry.

Government insiders tell me they anticipate one or perhaps two more big announcements in the coming months, most notably Jaguar Land Rover's Gigafactory decision. A series of new carmakers have been engaged for talks, including Tesla (which has already staked its main European base in Germany but is considering smaller factories), Rivian, Polestar and Canoo.

Local authorities and regional board around the country are pitching plans for gigafactories. Some are more serious than others.

An artist's impression of the Britishvolt site in Blyth

An artist's impression of the Britishvolt site in Blyth

But there are two problems.

The first is that Britishvolt remains a new, untested company, attempting to take on an Asian industry which has successfully dominated the sector for years. Only last year Johnson Matthey, the catalyst specialist which was until then one of the great hopes of the UK's nascent cell sector, abruptly pulled out of its plans to make battery materials.

In other words, turning these promises into reality remains difficult.

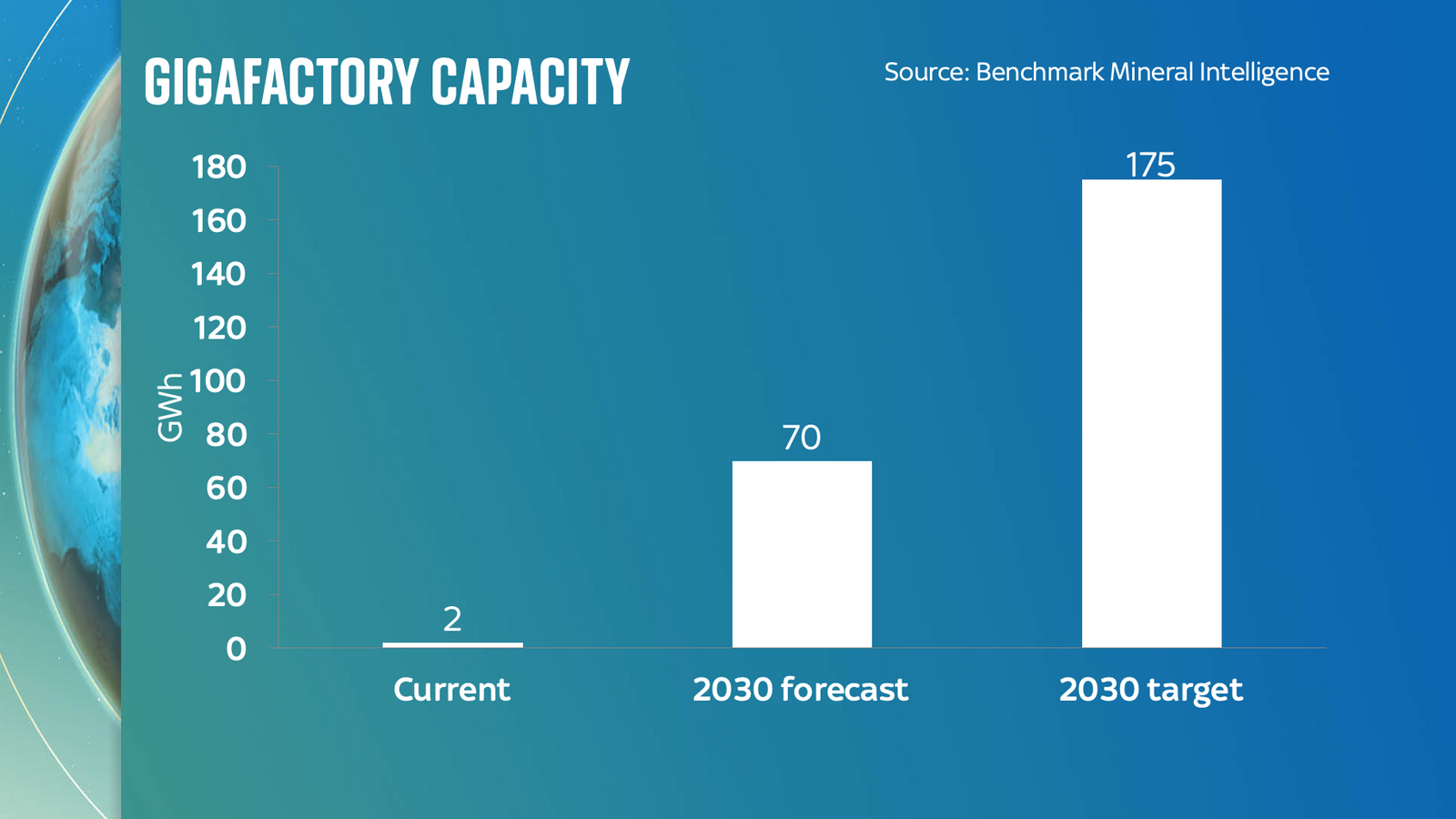

Nor is it obvious that the UK's battery ambitions are ambitious enough. According to a dossier of figures submitted privately to the Department for Business, Energy and Industrial Strategy and seen by Sky News, gigafactory capacity is forecast to be barely half the needed level by the end of the decade.

The data, from Benchmark Mineral Intelligence, one of the world's leading authorities on the battery industry and a member of the BEIS Critical Minerals Expert Committee, shows that by 2030, the year the government plans to ban the sale of internal combustion engine cars, it will have just short of 70 GWh of battery production, but that it should be targeting 175 GWh if it is to retain car production.

This latter target is also nearly double the government's informal target of 90 GWh.

The second problem is that it's all very well building a battery factory but that factory will need tonnes of raw materials out of which its batteries will be made. And there is a race under way to secure those materials - a race the UK is only now joining, years after the EU and US.

The London Metal Exchange

You get a sense of this race when you visit the floor of the London Metal Exchange, one of the few markets in the world where traders still meet in person for "open outcry" sessions, shouting at each other to determine the prices of metals like copper, nickel and aluminium.

The values of these commodities, important components of batteries, have yo-yoed dramatically in recent months as traders have attempted to calculate the impact of what many call the green industrial revolution.

According to investment bank Goldman Sachs, demand for copper - an essential metal for electrical wiring - could rise by 900% by 2030, an extraordinary and unprecedented increase.

Traders at the London Metal Exchange

Traders at the London Metal Exchange

There are big question marks over where this copper will come from, since global mining companies remain somewhat nervous about new mines, having suffered an almighty boom and bust in the past couple of decades.

Still, there is nothing especially novel about copper mining; indeed, it is one of the oldest industries in the world.

A more testing question is how the world is going to get the other, more obscure ingredients it will need to build the batteries it will need to electrify the world. Chief among those metals is lithium which is, as the name suggests, the most important ingredient in lithium ion batteries.

How are electric batteries made?

The electrochemistry of batteries is a fascinating and complex topic, so much so that it still baffles many in the industry. Nonetheless it is worth pondering what's going on inside a battery, since it is at heart about the interplay of certain very special elements.

At its simplest, a battery is composed of two main components: a cathode and an anode. In the case of a lithium ion battery, the lithium is mostly to be found in the cathode where it and a few other ingredients, most often cobalt and nickel, are powder-coated on to aluminium foil and rolled into a canister or layered in a kind of pouch.

The ingredients differ from battery to battery. In some, especially smartphone batteries, levels of cobalt are comparatively high. But since most of the world's cobalt comes from the Democratic Republic of Congo, where enormous questions remain about mining conditions and human rights, battery makers have been gradually reducing the quantity in their batteries.

In some battery chemistries - especially in those produced in China - there is no cobalt at all. But there is no escaping the need for lithium. This is because the lithium is the active ingredient in the electrochemical cadence underlying these cells. When the battery is charging up, lithium ions, which is to say electrically-charged atoms, move from the cathode to the anode, which is usually copper foil coated with graphite. When the battery discharges, they move back from the anode to the cathode.

This is all happening beneath the surface of your battery, which is to say that even if you could peer inside it you wouldn't see the lithium atoms moving. However if you looked very closely indeed what you might detect is that as the battery charges the size of the anode increases ever so slightly, as the lithium ions migrate and nestle into the atomic structure provided by the graphite.

This is, of course, a gross simplification since there is plenty else going on besides: there is a liquid electrolyte which also contains lithium and a separator, generally a kind of plastic, which keeps the cathode and anode apart. But if you remember one thing about the life of a battery, remember this rhythm: lithium ions traversing from one side to the other and then back again.

This electrochemical reaction was first discovered in 1980 by a team at Oxford University led by American chemist John B Goodenough. There is a blue hexagonal plaque commemorating the discovery on the side of the Inorganic Chemistry Laboratory just off the Parks Road in Oxford. Yet while the lithium ion battery was invented in the UK, the task of commercialising and mass producing them was taken up in the 1990s by Sony, which needed new rechargeable batteries for its camcorders and Walkmans.

The story of these batteries, the chief protagonists in the race to net zero, raises some testing questions: why did the UK, having invented the technology, then fail to build an industry around it?

Why is it still playing catch-up today, not just leagues behind Asian giants like China, Japan and South Korea, but also behind the US and EU, both of which are moving faster to build local battery supply chains?

Part of the answer comes back to the fact that while Japan's electronics industry thrived in the 1990s, Britain's was shrinking. There simply wasn't a mass market for the batteries.

It underlines an important point, something often lost amid woolly discussions about industrial strategy: it's all very well having the smartest folks or the best industrial processes but all too often what matters is proximity.

Japan built a battery industry in large part because it was also making the products into which those batteries are inserted.

This gravitational pull matters with many products but especially with batteries, which are classed as dangerous, combustible goods subject to many checks and trade barriers.

That brings us back to the car industry: one manufacturing trade where Britain is a genuine contender. It may not make Walkmans or camcorders but these days the main market for batteries is moving vehicles.

A record number of electric cars were sold in 2021

A record number of electric cars were sold in 2021

The other explanation for Britain's failure to capitalise on the invention of these batteries comes down to what people in politics call "industrial strategy".

It is going too far to say Britain has no industrial strategy. When it comes to certain sectors - cars, finance, defence - it has often dangled incentives in front of companies to encourage them to locate in the UK.

But unlike countries like South Korea or China or even Germany, Britain has tended to stop short of full-blooded strategic plans to set up a given sector.

Consider Taiwan's boldness in funding and enshrining a semiconductor industry over the past three decades and now consider whether anything of the sort would ever happen in the UK. You see the point.

But (hesitate as one might to use the words) might this time be different?

Perhaps it's because the motor industry is at the epicentre of the push for batteries. Perhaps it's because other countries are providing lavish incentives for battery startups. Perhaps there's a recognition that there's an opportunity here.

Either way, Whitehall is seemingly being forced out of its comfort zone, away from its default position of leaving the private sector to fend for itself. That goes for the question of subsidies for strategic industries.

Through a number of bodies - primarily the Advanced Propulsion Centre - the government is taking a more activist approach than anyone I've spoken to in the industry or indeed Whitehall can recall.

It has provided some of the funding for Britishvolt through its Automotive Transformation Fund and, via the Faraday Institution, is trying to encourage research in new battery technologies. And then there's the question of how to source the minerals needed by those industries.

Unlike the US or EU, Britain does not have a critical or strategic minerals strategy aimed at planning where it will get the materials necessary for these gigafactories and other plants manufacturing the products of the future.

To some extent this is because it was able, until Brexit, to piggyback on the European Commission's scheme. But a deeper explanation is that in recent decades such things - a government making central decisions about which metals and minerals we might or might not need - simply didn't seem compatible with the British economic model.

Meddling with such things seemed to bespeak some ancient form of economic mercantilism rather than the liberalism of Britain's services-first economy.

This is all about to change. The Department for Business, Energy and Industrial Strategy has convened a group of experts and business people and is working on creating its own list of critical minerals, to be published later this year.

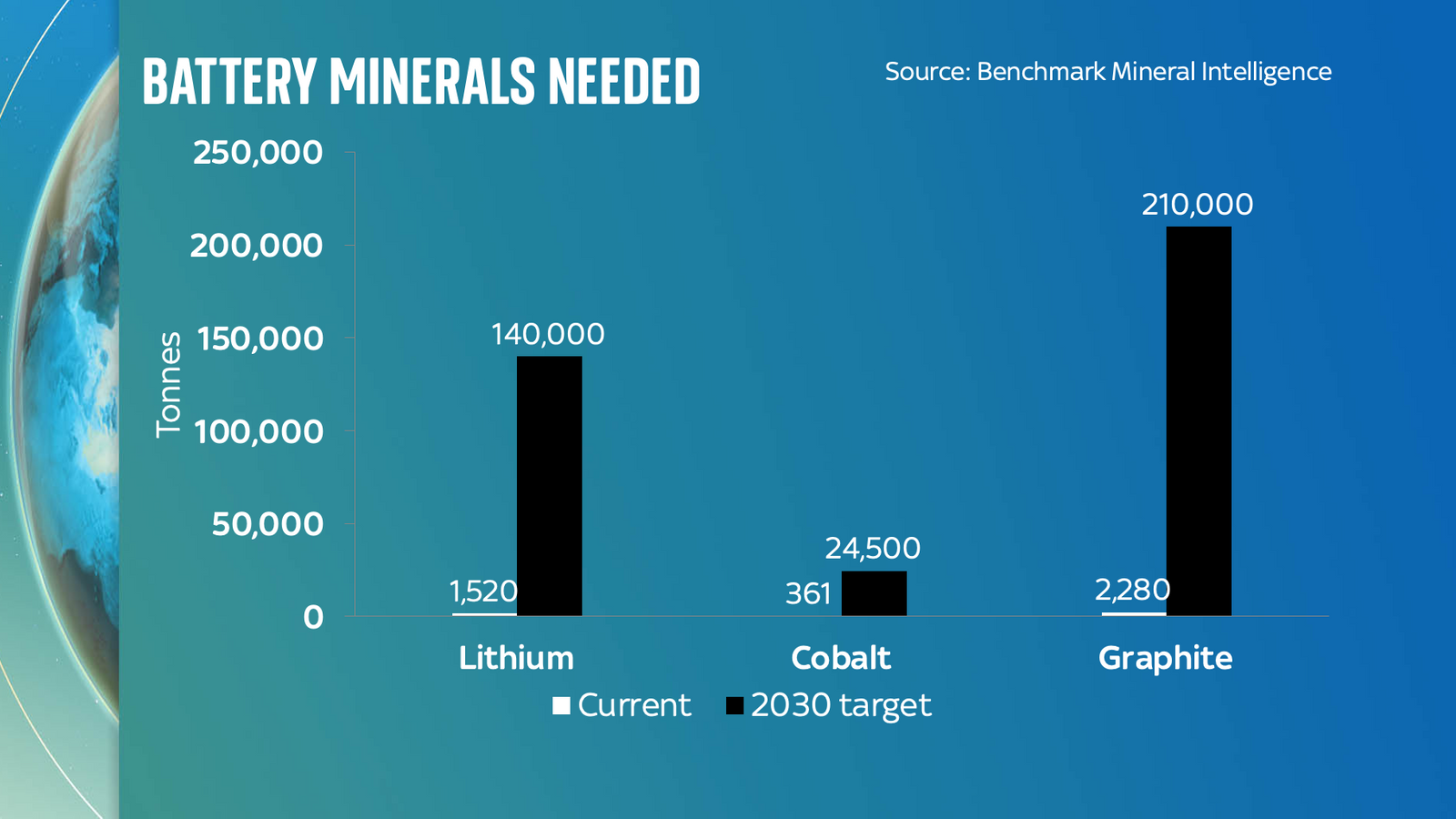

Among the members of that group is Benchmark Mineral Intelligence, which produced the dossier of data seen by Sky News. Its data also underlines the scale of physical materials the UK needs.

It projects that the UK's demand for lithium - the pivotal material in all mainstream rechargeable batteries - would rise from 1,500 tonnes this year to around 60,000 by 2030 on the basis of current gigafactory plans, and to 140,000 tonnes if the UK aims to increase its battery manufacturing in line with Benchmark's recommended target.

It is yet more food for thought as the government works on the creation of its critical minerals list and strategy.

Quite what is done with this list remains to be seen. Will the UK government begin building up stockpiles of lithium in warehouses around the country?

Will there be special tariff rates or subsidies for companies capable of supplying rare earth metals or phosphates or metallurgical silicon? My impression is that BEIS itself still doesn't have an answer.

However, it is running out of time to formulate one, for the race to secure these minerals is hotting up. You can see it in the prices of metals on the London Metal Exchange and beyond.

The price of lithium has shot up rapidly in recent months as demand for the metal has outpaced the likely supply coming down the pipeline.

Most of the world's lithium comes from two places: there is lithium from South America, pumped as brine out of the "salars" - salt lakes in Chile, Bolivia and Argentina.

And there is lithium from rocks found most notably in Australia.

Some of the Chilean lithium, notably the stuff extracted by SQM, the western world's leading producer, is refined locally. But much of it - especially the Australian rocks - are shipped off to China where it is refined and turned into the lithium carbonate and lithium hydroxide which then goes on to the cathodes in those batteries.

Britain has neither salars nor spodumene. But a few entrepreneurs have decided not to let that get in their way.

The British Lithium Pilot in St Austell

This being January and this being Cornwall, this part of the country is smothered in a permafog when we visit the St Austell home of British Lithium.

The fog is so thick you can barely make out the quarry where this company is planning to extract rock, out of which it will extract lithium. We are, in other words, a long way from the deserts of Australia or the high deserts of Chile.

Yet British Lithium is one of two companies attempting a new kind of lithium mining. It is planning to extract lithium from a kind of granite which sits beneath much of Cornwall.

The concentration of lithium is admittedly far smaller than those other sources, but in its pilot project British Lithium has already managed to produce bags and bags of lithium carbonate, pure enough to go into a battery cathode (or be converted into the lithium hydroxide some battery makers prefer).

The British Lithium Pilot plant in St Austell

The British Lithium Pilot plant in St Austell

With lithium prices soaring, suddenly the numbers, even for projects like this which focus on unusual resources, look attractive.

But the project here - and nearby Cornish Lithium, which is also planning to extract a bit of lithium brine as well as rock - also raises a deeper question: if Britain is going to produce its own batteries does that mean it should also be producing its own battery materials?

Andrew Smith, BL's chief executive, declares that his site could, within a few years, produce a third of the country's lithium.

Not long ago such projects might have been dismissed by the Treasury, which tends to opt for the cheapest possible deal, wherever in the world it might be. But in an era when gas prices are soaring and politicians are panicking about energy security, might that price-first strategy seem a little short-sighted?

Andrew Smith from the British Lithium Pilot talks to Ed Conway

Andrew Smith from the British Lithium Pilot talks to Ed Conway

In the space of the past few months Mr Smith has turned this from an empty hangar into a production line - crushers and conveyors and tanks and calciners - doing something rather special: wringing lithium out of Cornish rock.

When I visit he has covered some of the machines with tarpaulins and hurriedly shows us which bits we cannot film: this control panel and that tank. They look rather unremarkable to my untrained eyes but, he insists, were this glimpse to find its ways to the wrong eyes then trade secrets could rapidly find their way to the other side of the world.

And given we are in the early stages of a gold rush - a white gold rush for the glistening powder of lithium salts - you can see his point.

If we are to increase the number of battery electric vehicles by twenty-fold in the coming decades then we will need a 2,000 per cent increase in the amount of lithium we're getting out of the ground.

Can Britain reduce its reliance on lithium?

In the face of such a challenge perhaps it's no surprise that some are trying to work out how to reduce our reliance on lithium.

One start-up to watch is Sheffield-based Faradion, one of the world leaders in an exciting new battery technology: sodium ion. Sodium is, like lithium, light and reactive. Like lithium it works well in a cathode - the business end of a battery. But unlike lithium, sodium is plentiful. You can even extract it from table salt (sodium chloride).

There are other advantages: sodium ion batteries are significantly safer than lithium ion ones, less prone to catching on fire if something goes wrong.

There is a catch too: they hold less charge than their lithium counterparts. Still: given the concerns about getting enough lithium out of the ground, perhaps new batteries like this might hold promise for the future.

According to Professor Peter Bruce of Oxford University, one of the world's leading battery experts, this is just one field of research where Britain has a fighting chance to invent world-beating technology again. There are solid state batteries, lithium sulphur, even lithium air. The "arms race" - as James Quinn, chief executive of Faradion calls it - is getting very serious indeed.

But it's hard to escape the importance of lithium. Which brings us to another question. Let's say British Lithium is successful and manages to extract enough lithium.

Let's say Britishvolt builds a brilliant gigafactory. What happens in between those two places? The answer is all-important yet it's not altogether clear those in Whitehall have done much thinking about it.

For it turns out you can't just take lithium, or for that matter lithium carbonate or lithium hydroxide, and dump them into Britishvolt's factory.

In between these two parts of the supply chain is another step: converting that lithium into the magic substance that forms the cathode in the battery.

Cathode active materials is a whole speciality in and of itself. It takes a lot of expertise and IP to take lithium, cobalt, nickel and a few other critical minerals and mix them in the right way to turn out a cathode.

And while there are a few big players in the game in Europe - most notably Umicore of Belgium - the UK does not have a pawn in this game. Not anymore. Not since Johnson Matthey, the catalytic converter manufacturer, unexpectedly pulled out of the sector.

This is, to put it lightly, problematic. It is all very well having a fleet of gigafactories. It is all very well having lithium from Cornish stone.

But if the cathodes and, as we'll get to in a second, the anodes, are made outside of Europe, then those rules of origin requirements which determine whether an exported car benefits from special tariff deals suddenly come back to bite the UK.

This is the great gaping hole in the UK's battery strategy, and while a few people within the agencies who look at this are trying hard to shout this message to Downing Street, it is not obvious anyone is listening.

Indeed, it's not obvious anyone there realises that even as we attempt to build out the UK's battery supply chain, a critical link has been hiding in plain sight, in this country, all along. Which takes us back to where we started.

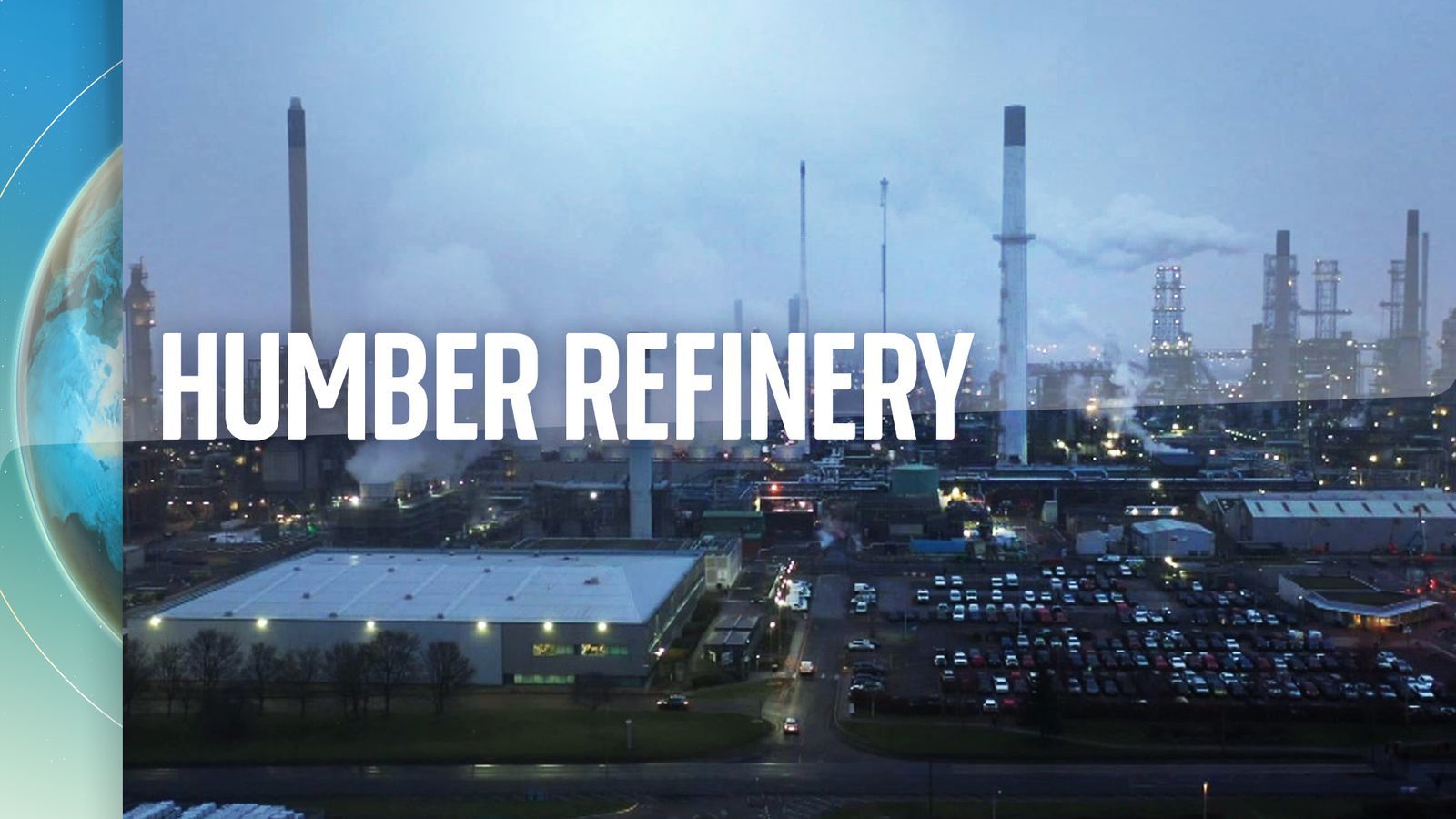

The Humber Refinery in Immingham

The temperature is just below freezing on the January morning we visit the Humber Refinery, but as we walk through the plant every so often we are blasted with a burst of steam from one of the pipes which briefly warms the cockles.

We have been issued with flame retardant suits and at every corner we pass there is a shower which can douse you with water if there is an accident. Our phones have been confiscated, along with any unauthorised piece of machinery which could spark a fire. An occasional hazard of lithium ion batteries.

Having covered the economy for some years, I am moderately good at recognising heavy machinery when I see it: a rotary kiln here, a heavy steel press there. Refineries, on the other hand, have always been more befuddling.

What is this pipe for? What does this tank do? I mention this to one of our guides, who gently puts me in my place by telling me that when he drives past a refinery he instantly knows what they're making. He points at a couple of scaffolds above one of the tanks.

"These drilling rigs," he says, "well, they're a dead giveaway about what's going on here." I stare at the scaffolds for a moment, nonplussed.

What do they make at the Humber Refinery?

Where to begin? Perhaps with crude oil, the main feedstock. It comes in, mostly from the North Sea, is scrubbed and cleaned, the saltwater removed, and from lightest to heaviest, the hydrocarbon products are extracted. There is propane for heating and transportation; propylene which forms the basis of many plastics; butane for heating; benzene, the basis of everything from rubbers and dyes to pharmaceuticals and pesticides; naphtha and petrol (a fifth of the UK's supply), aviation fuel and kerosene, diesel and gasoil.

But for our purposes the most intriguing product is the one that comes out from beneath these drilling rigs, deep inside the refinery. Here, day and night, they bake some of the heaviest parts of the crude oil - quite literally the bottom of the barrel - drill out what is left with extraordinarily high-pressure water drills, run the resulting product through kilns and out come dark, grey-black pockmarked pebbles which look a little bit like miniature asteroids.

This is coke, a dry, light, very carbon-heavy mineral. You've probably heard of coke before. The most well-known variety is coking coal, made from the coal you dig from the ground and used to make steel from iron ore. But the coke they make here at this refinery, owned by American company Phillips 66, is very special indeed. It goes by a few names: needle coke, premium coke, graphite coke and they have been making it here for decades. But in the past few years, it has suddenly become very important indeed.

For after the coke is churned out of the kilns here, it is shipped overseas, mostly to China. There it is cooked at high temperatures in a further process which turns it into an incredibly pure form of graphite - sheet upon sheet of carbon atoms. This so-called synthetic graphite is then mixed with the "natural" graphite you get out of the ground and turned into a fine powder which is then coated on to fine copper sheets. Lo and behold, the coke which came out of the Phillips 66 refinery has become an anode.

That's right: one of the critical materials going into batteries today is a processed form of crude oil, much of it coming from the North Sea. There are a few grams of Humberside coke in many if not most smartphones in the world, sitting alongside the lithium and cobalt, without which those batteries simply wouldn't function.

Much is made these days about the lithium inside batteries or the cobalt that also goes into the cathodes. Far less is said about the other end of the battery. Yet without the kind of graphite produced from Humberside coke (and this refinery turns out to be one of the world's most important producers of the stuff - and the only one in Europe) net zero will remain a pipe dream.

Why? Because it turns out that without synthetic graphite, batteries simply don't work as well. The lithium ions which spend their lives floating from cathode to anode fly across far faster when there is a decent proportion of synthetic graphite in the anode. Put simply, synthetic graphite is what helps phones and for that matter electric cars to charge rapidly.

At this stage perhaps you are wondering why you haven't previously heard of the Humber Refinery. After all, this turns out to be one of the most important links in the supply chain for the most important product of the green industrial revolution.

And the UK happens to have one of the world's biggest producers of the stuff. Why aren't we shouting about this even more?

Perhaps, bluntly, it's because of the way this refinery looks from the outside: an impenetrable fossil fuel fortress. Perhaps it's because no one much likes to discuss the fact that you need crude oil to make batteries, or that you need a dirty, energy-intensive set of processes to process it into the coke and then the graphite that make the world's batteries work.

Are the "optics" simply a bit too challenging?

Coke pits at the Humber Refinery

Coke pits at the Humber Refinery

Perhaps. Either way, Humberside's expertise at making this particular type of coke hasn't gone unnoticed elsewhere.

A couple of years ago a Chinese spy was uncovered working deep in Phillips 66's headquarters in Oklahoma. Hongjin Tan was discovered downloading hundreds of electronic blueprints on to a USB stick, to take back to manufacturers in China.

The intellectual property he was looking for? The recipes and techniques used here in Humberside to make the coke that feeds the battery supply chain.

It raises a deeper issue. Some in China, which already controls many parts of the battery supply chain, will stop at nothing to dominate this business completely.

Yet even as they do so, the British government remains somewhat unfocused, to put it gently, on how best to capitalise on the areas where the UK has a competitive advantage.

There is a vision of the future where the UK has a genuine edge in battery production, but the reality is it's unlikely to be in the fields where it is already so far behind everyone else.

This country is unlikely to outdo Germany on gigafactories. It is unlikely to compete with Belgium's Umicore on cathode materials. It is unlikely, despite the best efforts of British Lithium, to outdo Chile or Australia.

But it could plausibly be the most important hub in Europe for anode production. If there were a factory beside this refinery turning the coke here into anodes, which are then sent a few hundred miles up north to Britishvolt, well then a lot of Britain's problems might be answered.

Yet at the moment such an idea remains a pipe dream. The main reason Humberside coke is sent off to the other side of the world, before being sold back into this country as a Chinese import, is that British producers simply cannot compete with China on energy prices and labour costs.

And while the processes here are part of the route towards net zero, ironically enough that vision of an anode materials plant next door to this refinery would involve, guess what, even more domestic carbon emissions.

Such are the paradoxes one encounters as one burrows deeper into the world of batteries. Here, at the heart of the green industrial revolution, are challenges and opportunities aplenty. Whether they are widely comprehended, let alone pursued, is another matter.